LLC vs Corporation In North Carolina - 2025

Understanding LLCs and Corporations

An LLC and a corporation are both popular business structures in North Carolina. They each have their own unique features, especially in terms of liability protection, management, and taxation. This section will explore the key characteristics that define these business entities.

Definition and Characteristics of LLC

A Limited Liability Company (LLC) is a business entity that combines the liability protection of a corporation with the tax benefits of a partnership. LLCs offer flexibility and are popular for small businesses because they protect members' personal assets from business debts.

LLCs in North Carolina can be managed by their members or by managers. This means the day-to-day operations can be run by the owners or a hired manager. This structure provides adaptability, which is attractive to many business owners.

Taxes for LLCs are typically passed through to the individual members, avoiding the double taxation seen in C corporations. Members report the business's income on their personal tax returns.

For more detailed information about the legal structure of LLCs in North Carolina, visit starting an LLC in North Carolina.

Definition and Characteristics of a Corporation

A corporation is a structured business entity recognized as a separate legal entity from its owners. This structure provides limited liability to shareholders, meaning their personal assets are generally protected from business liabilities.

Corporations can be either C corporations or S corporations, each having its own tax implications. C corporations face double taxation, where income is taxed at both the corporate level and again on shareholders' personal tax returns. S corporations avoid this by passing income directly to shareholders.

In North Carolina, corporations adhere to a stricter management structure, typically involving a board of directors and officers. This formality can appeal to businesses looking for a clear, established hierarchy in management.

For more insights on business structures, refer to choose a business structure at the North Carolina Secretary of State website.

Formation and Registration in North Carolina

Starting a business in North Carolina involves specific steps based on whether the business is registered as a limited liability company (LLC) or a corporation. This section highlights the important processes for both business structures and what is required to register them legally.

LLC Formation Process

Forming an LLC in North Carolina begins with choosing a unique business name. The name must include "Limited Liability Company” or an abbreviation like "LLC." It cannot be similar to existing business names in the state. After selecting the name, the next step is preparing and filing the Articles of Organization.

A registered agent is necessary and must be a resident of North Carolina or a business entity authorized to operate in the state. This agent receives legal documents on behalf of the LLC. Filing the Articles of Organization with the Secretary of State requires a filing fee.

The LLC becomes official once these documents are filed and approved. To maintain good standing, LLCs need to file annual reports and pay associated fees.

Corporation Formation Process

The corporation formation process in North Carolina starts with choosing a business name, which should include "Corporation," "Incorporated," or an appropriate abbreviation. The business name must be distinguishable from others. Filing the Articles of Incorporation with the Secretary of State is crucial.

This filing requires a set fee and outlines the corporation's essential details, including corporate bylaws, stock information, and the registered agent's contact details. The registered agent must be available during business hours.

Like LLCs, corporations must submit annual reports. These reports ensure compliance with state laws. Remaining diligent with these filings helps maintain the corporation’s active status in North Carolina.

Ownership and Management

In North Carolina, differences in ownership and management between LLCs and corporations influence decision-making, operational control, and business dynamics. The specifics of these structures determine how businesses are governed and managed.

LLC Management Structure and Flexibility

Limited Liability Companies (LLCs) in North Carolina offer a flexible management structure. LLCs can be either member-managed or manager-managed. In a member-managed LLC, the owners actively handle daily operations. This setup allows owners direct control over the business, ideal for small teams or single-owner businesses.

A manager-managed LLC appoints a separate manager to take charge of business operations. This approach frees owners from daily tasks, making it suitable for larger businesses or passive investors.

The LLC's management style is usually outlined in an operating agreement, a document detailing rights, duties, and operating procedures. This flexibility allows an LLC to adapt its management according to its unique needs, emphasizing simplicity and owner preference.

Corporate Management and the Board of Directors

Corporations in North Carolina have a more formal management structure. They are governed by a board of directors, elected by the shareholders. The board oversees major decisions, while officers handle daily tasks. This separation ensures structured and clear governance.

Shareholder influence is exerted through voting rights, typically determined by the number of shares held. Corporate bylaws outline the specific roles, responsibilities, and rules, ensuring transparency and consistency in management.

Unlike LLCs, the corporate structure is less flexible but provides clear accountability. The board's decision-making is geared toward maximizing shareholder value. This structured hierarchy can attract investors looking for a regulated and predictable management environment, as explained in LLC vs Corporation: How Are They Different?.

Liability and Legal Protections

When choosing between an LLC and a corporation in North Carolina, understanding liability protection is crucial. Both LLCs and corporations provide some form of limited liability, shielding personal assets from business liabilities. However, they differ in how they achieve this protection.

Limited Liability Protection in LLCs

Limited Liability Companies (LLCs) offer significant protection for personal assets. This means that if an LLC faces legal claims or debts, the owners—referred to as members—are generally not personally accountable. Their personal assets, like homes or cars, remain protected from business creditors.

LLCs are governed by an Operating Agreement, which outlines how the company will be managed. This flexibility appeals to small business owners who prefer direct involvement in day-to-day operations. It's important to note that while LLCs provide protection from business liabilities, members should ensure they do not personally guarantee business debts to maintain this limited liability protection.

Corporate Shield and Personal Liability

Corporations offer a robust legal structure called the corporate shield, which protects personal assets from business liabilities. Shareholders are not personally liable for corporate debts or legal obligations. This structure is typically governed by Bylaws, and it often involves a board of directors who set policies and make major decisions.

The corporate shield is an attractive feature for entrepreneurs planning to seek external investors. It assures that their personal exposure to risk remains minimal. However, maintaining this shield requires strict adherence to corporate formalities, such as regular board meetings and accurate record-keeping. This formality helps ensure that personal liability is kept separate from business liability, providing legal liability protection.

Taxation Differences and Implications

Taxation for business structures can greatly impact financial outcomes. While LLCs and corporations both operate within North Carolina, they face different tax treatments and responsibilities.

Pass-Through Taxation in LLCs

Limited Liability Companies (LLCs) enjoy pass-through taxation. This means that profits and losses are reported on the personal tax returns of the owners. LLC members pay taxes on their share of the income, which helps avoid double taxation. For instance, instead of being taxed at both the corporate and personal level, as C-corporations experience, LLC members deal only with personal tax rates.

This can lead to tax advantages for LLC owners, particularly small businesses. There is also no requirement to pay self-employment taxes on the entire profit if the LLC elects to be taxed as an S-corporation. Electing S-corp status may result in reduced taxes on income distributions, providing further financial benefits.

Corporate Taxation and Double Taxation

Corporations, including C-corporations, are taxed differently. Profits are taxed at the corporate level when earned, and again at the shareholder level when dividends are distributed. This phenomenon is known as double taxation. To choose corporate tax treatment, a corporation must file IRS Form 2553.

In North Carolina, corporations are subject to both state corporate income tax and a franchise tax. The franchise tax applies every year and is filed with Form CD-405. However, there’s an elective tax option for S-corporations, which could eliminate double taxation. S-corporations can minimize overall tax burdens by allowing income to pass through to shareholders directly, similar to LLCs. Businesses should consider these tax classifications carefully to optimize their tax strategy.

For more detailed comparisons, check out the article on LLC vs S-Corp in North Carolina.

Administrative Requirements and Compliance

In North Carolina, LLCs and corporations must adhere to specific administrative requirements to maintain good standing. These requirements involve annual reports and record-keeping protocols to ensure compliance with state regulations.

Annual Reports and Ongoing Formalities for LLCs

LLCs in North Carolina must file an annual report with the Secretary of State. This report includes essential information like the LLC’s name, principal office address, and member details. Filing fees are associated with this report, and timely submission is crucial to avoid penalties.

LLCs benefit from having fewer formal meeting requirements than corporations. However, maintaining accurate financial records and a clear outline of ownership and member responsibilities is vital. This ensures smooth operation and can help in resolving disputes.

It's important for LLCs to comply with state regulations consistently. Missing deadlines or requirements can result in the LLC being administratively dissolved, causing potential operational disruptions.

Corporate Record Keeping and Compliance

Corporations must maintain detailed records, including bylaws, meeting minutes, and financial statements. Unlike LLCs, corporations are required to hold annual shareholder and board meetings. These meetings help ensure accountability and transparency in operations.

Maintaining meticulous records is crucial for compliance with North Carolina state laws. Corporations must also submit an annual report, much like LLCs, but the specifics can vary. Filing fees and deadlines apply, with the need for diligence to prevent penalties.

Corporations also have the option to elect S corporation status for tax purposes. This requires additional documentation and compliance with Tax Characteristics. Failing to keep up can result in legal complications or financial penalties.

Considerations for North Carolina Small Businesses

Choosing between an LLC and a Corporation in North Carolina involves important factors like ease of management, taxation, and liability. Seeking professional advice can assist in making the best choice for your business needs.

Choosing the Right Entity for Your Business

Small business owners in North Carolina have several choices when it comes to forming a business entity. Many opt for a North Carolina LLC due to its simplicity and flexibility. An LLC allows for various tax treatments and requires less paperwork than a corporation. This makes it an appealing option for those starting a small business.

However, corporations offer benefits like attracting investors and allowing stock options. This could be important for businesses aiming for rapid growth. Sole proprietorships are another option, though they offer less protection than LLCs or corporations. The right choice depends on the specific needs of the business and the vision of the owner. Comprehensive guidance on business entity options in North Carolina is available online for detailed insights.

Professional Guidance and Legal Assistance

Engaging an attorney can provide valuable insights into forming and managing a business entity. Lawyers can help navigate legal requirements and ensure compliance with North Carolina's laws. They can also assist in understanding tax implications.

Legal professionals are well-versed in the requirements for setting up different entities. This can be especially helpful for small businesses. For those considering forming a North Carolina LLC or corporation, exploring professional services like those offered by the Law Offices in Matthews can be beneficial. Such assistance ensures the business is set up correctly from the start, saving time and avoiding potential issues down the road.

Frequently Asked Questions

Understanding the differences between LLCs and corporations in North Carolina involves considering tax implications, costs, and structural elements. This section explores common questions about these business forms in North Carolina, providing key insights to help in deciding which one to choose.

What are the tax implications for LLCs versus corporations in North Carolina?

In North Carolina, an LLC benefits from pass-through taxation, meaning profits are reported on the owners' tax returns. A corporation pays a corporate income tax. An S Corporation can elect similar tax treatment as an LLC, avoiding double taxation.

Can you outline the advantages and disadvantages of forming an LLC compared to a corporation in North Carolina?

LLCs offer flexibility and simple management structure with limited liability protection. Corporations provide easier access to capital and established governance. LLCs generally have fewer compliance requirements, while corporations have more complex regulations. Each has unique benefits depending on business goals.

What are the costs associated with establishing an LLC versus a corporation in North Carolina?

The state filing fee for forming an LLC or a corporation in North Carolina is similar. Out-of-state entities pay additional fees. Ongoing costs may include annual reports and any additional services like legal or accounting advice. Check the North Carolina Secretary of State for accurate fee details.

How does setting up a corporation in North Carolina differ from creating an LLC?

Setting up an LLC involves filing articles of organization and creating an operating agreement. A corporation requires more documentation, such as articles of incorporation and corporate bylaws. Corporations need to appoint directors and hold regular meetings.

What are the key differences between the officials required for NC LLCs and corporations?

LLCs typically have members or managers, while corporations have shareholders, directors, and officers. Each role has specific duties and responsibilities. Members of an LLC can manage the business directly, but a board oversees a corporation.

What distinct types of LLCs can be formed in North Carolina and how do they vary?

North Carolina allows for standard LLCs, professional LLCs (for licensed professionals), and series LLCs, which provide separate liability for different units under one entity. Each type serves different business needs, affecting liability and operational flexibility.

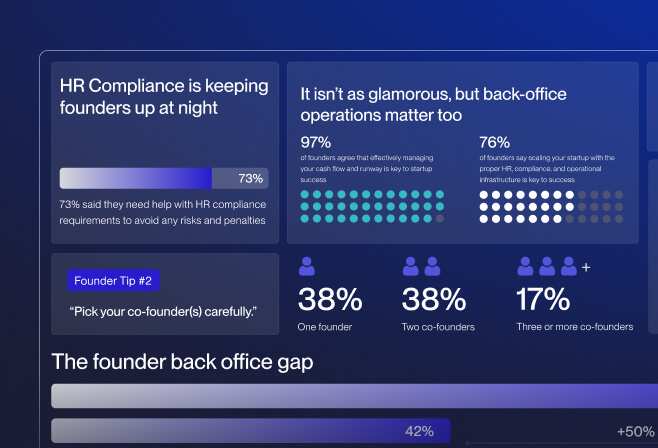

Up to 3,500 bonus and 3% cash-back on all card spend [3], 6 months off payroll, and 50% off bookkeeping for 6 months, free R&D credit.

Frequently Asked Questions

- How do I sign up for Every?

You can get started right away—just click “Get Started” and follow a short onboarding flow. Prefer a little help? One of our specialists can walk you through incorporation, banking, payroll, accounting, or whatever you need.

- What features does Every offer?

Every gives startups a complete back office in one platform. From incorporation and banking to payroll, bookkeeping, and tax filings, we take care of the operational heavy lifting—so you can spend more time building, less time managing.

- How is Every different from other tools?

Most competitors give you software. Every gives you a full-stack finance and HR team—plus smart financial tools that actually benefit founders. Earn up to 4.3% interest on idle cash and get cash back on every purchase made with your Every debit cards, routed straight back to you.

Every is not a bank. Banking services provided by Thread Bank, Member FDIC. Your deposits qualify for up to $3,000,000 in FDIC insurance coverage when Thread Bank places them at program banks in its deposit sweep program. Pass-through insurance coverage is subject to conditions. The Every Visa Business Debit Card is issued by Thread Bank, Member FDIC, pursuant to a license from Visa U.S.A. Inc. and may be used anywhere Visa cards are accepted.

- Is my data secure with Every?

We use end-to-end encryption, SOC 2-compliant infrastructure, and rigorous access controls to ensure your data is safe. Security isn’t a feature—it’s foundational.

Can I switch to Every if my company is already set up?Yes—you can switch to Every at any time, even if your company is already incorporated and running. Whether you're using separate tools for banking, payroll, bookkeeping, or taxes, we’ll help you bring everything into one place. Our onboarding specialists will guide you through the process, make sure your data is transferred cleanly, and get you set up quickly—without disrupting your operations. Most founders are fully transitioned within a week.

- What stage of startup is Every best for?

Every is designed for startups from day zero through Series A and beyond. Whether you're just incorporating or already running payroll and managing expenses, we meet you where you are. Early-stage founders use Every to get up and running fast—with banking, payroll, bookkeeping, and taxes all handled from day one. Growing teams love how Every scales with them, replacing patchwork tools and manual work with a clean, unified system.

We’re especially valuable for teams who want to move fast without hiring a full finance or HR team—giving founders more time to build, and fewer distractions from admin and compliance

- How long does onboarding take?

Onboarding with Every is fast and efficient. For most startups, the process typically takes between 3 to 7 days, depending on your specific needs and how much setup you already have in place.

If you're a new company, you'll be up and running quickly—getting your banking, payroll, and bookkeeping set up without hassle. If you’re transitioning from another system, our specialists will help you migrate your data, ensuring a smooth switch with no gaps or errors in your operations.

We guide you every step of the way, from incorporation to setting up automated payroll to handling your taxes—so you can focus on growing your business. Our goal is to make sure you're fully operational and confident in your back office in under a week.

Practical Questions to Ask to Ensure Your Bank is Well Managed

How much liquidity does the bank have on hand to cover unexpected withdrawals or shortfalls?

What percentage of the bank's deposits are invested in longer-term securities and loans, and what percentage is kept as cash reserves?

How does the bank diversify its investment portfolio to minimize potential losses and reduce risks?