SVB’s collapse explained in 6 steps

.png)

The story of Silicon Valley Bank (SVB) serves as a cautionary tale for other banks, highlighting the dangers of investing too heavily and having insufficient liquidity. In the years 2020 to 2022, SVB received an influx of deposits that they maximized by investing in longer-term securities and loans during the low-interest environment. However, when customer withdrawals and high-interest rates hit them hard, they found themselves with a liquidity crisis. This story covers the fall of SVB illustrated through data.

The data for this article comes from BankRegData, which sources data from the Quarterly Call Reports that each bank is required to report to their Regulator each quarter.

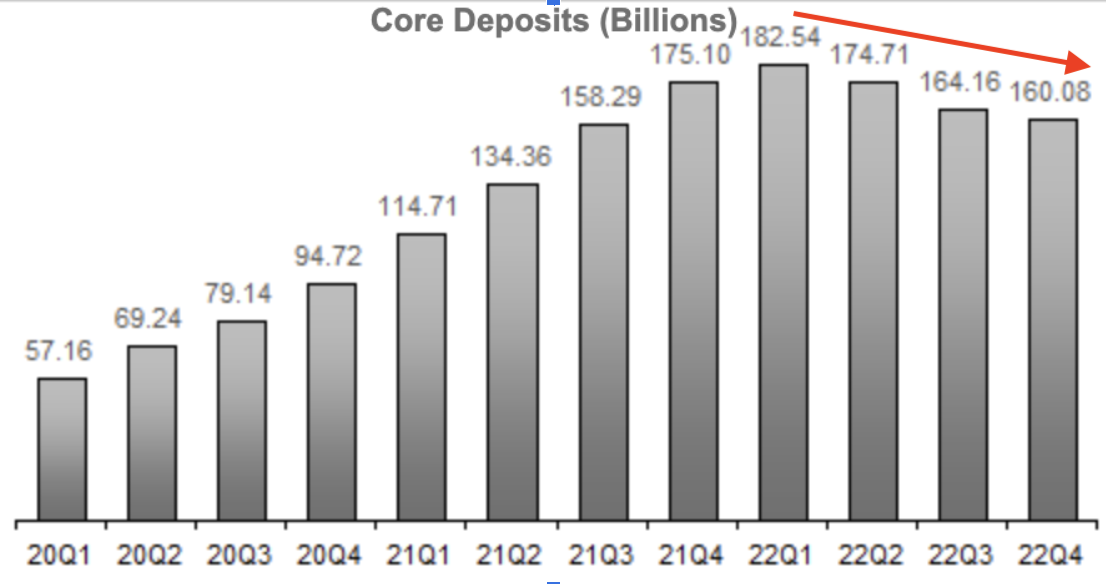

1. Between Quarter 1 2020 and Quarter 1 2022, SVB's deposits increased by $125 billion amid the massive influx of money to VCs investing in startups using SVB.

2. Where did SVB keep those deposits? 56% went to securities, 35% was loaned out to maximize their yield, and 6% remained as cash on hand.

3. Then, as you can see in the first graph SVB had an outflow of deposits from Quarter 1 2022 to Quarter4 2022, with a decrease in $22 billion in deposits which they needed to pay back to customers.

4. Why did this outflow happen? In addition to the change in the VC fundraising climate, as the interest rate increased in 2022, companies could put their money in US treasuries and get a risk-free high yield - where in contrast SVB was giving out .05-1.24% at this time.

During 2021's near zero interest rate environment, SVB locked their money in longer-term securities to garner a higher yield.

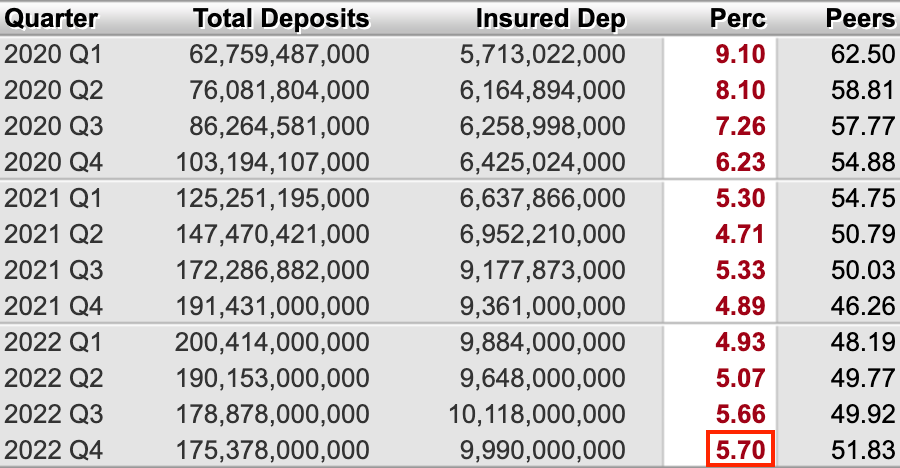

5. Because SVB invested the majority of its cash into long-term securities and loans to maximize its yield, they did not have enough cash on hand to pay back these withdrawals. They needed to pay back $22 billion but only had $12.5 billion cash on hand.

Below you can see how SVB borrowed;

6. SVB's announcement of a $1.75 billion capital raise led to widespread panic, particularly because the vast majority of the funds they held were uninsured, with less than 6% being covered. Ultimately, this led to the downfall of SVB.

Practical Questions to Ask to Ensure Your Bank is Well Managed

- How much liquidity does the bank have on hand to cover unexpected withdrawals or shortfalls?

- What percentage of the bank's deposits are invested in longer-term securities and loans, and what percentage is kept as cash reserves?

- How does the bank diversify its investment portfolio to minimize potential losses and reduce risks?

- How does the bank manage credit risk and ensure the creditworthiness of its borrowers?

- What is the bank's strategy for managing interest rate risk?

- What percent of deposits are insured?

- What measures does the bank have in place to ensure the safety and security of customer deposits?

Special thanks to Bill Moreland from BankRegData

Up to 3,500 bonus and 3% cash-back on all card spend [3], 6 months off payroll, and 50% off bookkeeping for 6 months, free R&D credit.

Frequently Asked Questions

- How do I sign up for Every?

You can get started right away—just click “Get Started” and follow a short onboarding flow. Prefer a little help? One of our specialists can walk you through incorporation, banking, payroll, accounting, or whatever you need.

- What features does Every offer?

Every gives startups a complete back office in one platform. From incorporation and banking to payroll, bookkeeping, and tax filings, we take care of the operational heavy lifting—so you can spend more time building, less time managing.

- How is Every different from other tools?

Most competitors give you software. Every gives you a full-stack finance and HR team—plus smart financial tools that actually benefit founders. Earn up to 4.3% interest on idle cash and get cash back on every purchase made with your Every debit cards, routed straight back to you.

Every is not a bank. Banking services provided by Thread Bank, Member FDIC. Your deposits qualify for up to $3,000,000 in FDIC insurance coverage when Thread Bank places them at program banks in its deposit sweep program. Pass-through insurance coverage is subject to conditions. The Every Visa Business Debit Card is issued by Thread Bank, Member FDIC, pursuant to a license from Visa U.S.A. Inc. and may be used anywhere Visa cards are accepted.

- Is my data secure with Every?

We use end-to-end encryption, SOC 2-compliant infrastructure, and rigorous access controls to ensure your data is safe. Security isn’t a feature—it’s foundational.

Can I switch to Every if my company is already set up?Yes—you can switch to Every at any time, even if your company is already incorporated and running. Whether you're using separate tools for banking, payroll, bookkeeping, or taxes, we’ll help you bring everything into one place. Our onboarding specialists will guide you through the process, make sure your data is transferred cleanly, and get you set up quickly—without disrupting your operations. Most founders are fully transitioned within a week.

- What stage of startup is Every best for?

Every is designed for startups from day zero through Series A and beyond. Whether you're just incorporating or already running payroll and managing expenses, we meet you where you are. Early-stage founders use Every to get up and running fast—with banking, payroll, bookkeeping, and taxes all handled from day one. Growing teams love how Every scales with them, replacing patchwork tools and manual work with a clean, unified system.

We’re especially valuable for teams who want to move fast without hiring a full finance or HR team—giving founders more time to build, and fewer distractions from admin and compliance

- How long does onboarding take?

Onboarding with Every is fast and efficient. For most startups, the process typically takes between 3 to 7 days, depending on your specific needs and how much setup you already have in place.

If you're a new company, you'll be up and running quickly—getting your banking, payroll, and bookkeeping set up without hassle. If you’re transitioning from another system, our specialists will help you migrate your data, ensuring a smooth switch with no gaps or errors in your operations.

We guide you every step of the way, from incorporation to setting up automated payroll to handling your taxes—so you can focus on growing your business. Our goal is to make sure you're fully operational and confident in your back office in under a week.

Practical Questions to Ask to Ensure Your Bank is Well Managed

How much liquidity does the bank have on hand to cover unexpected withdrawals or shortfalls?

What percentage of the bank's deposits are invested in longer-term securities and loans, and what percentage is kept as cash reserves?

How does the bank diversify its investment portfolio to minimize potential losses and reduce risks?

.png)