The Founder's Guide to Cutting Health Insurance Costs Without Cutting Coverage

Most founders don't think about health insurance until they have to. Then they get their first renewal quote, watch the number go up 7% for the third year in a row, and wonder if there's a better way.

There is. But most benefits brokers won't tell you about it — because it requires a type of platform that almost no one has built yet.

Health insurance costs are out of control — and they keep climbing

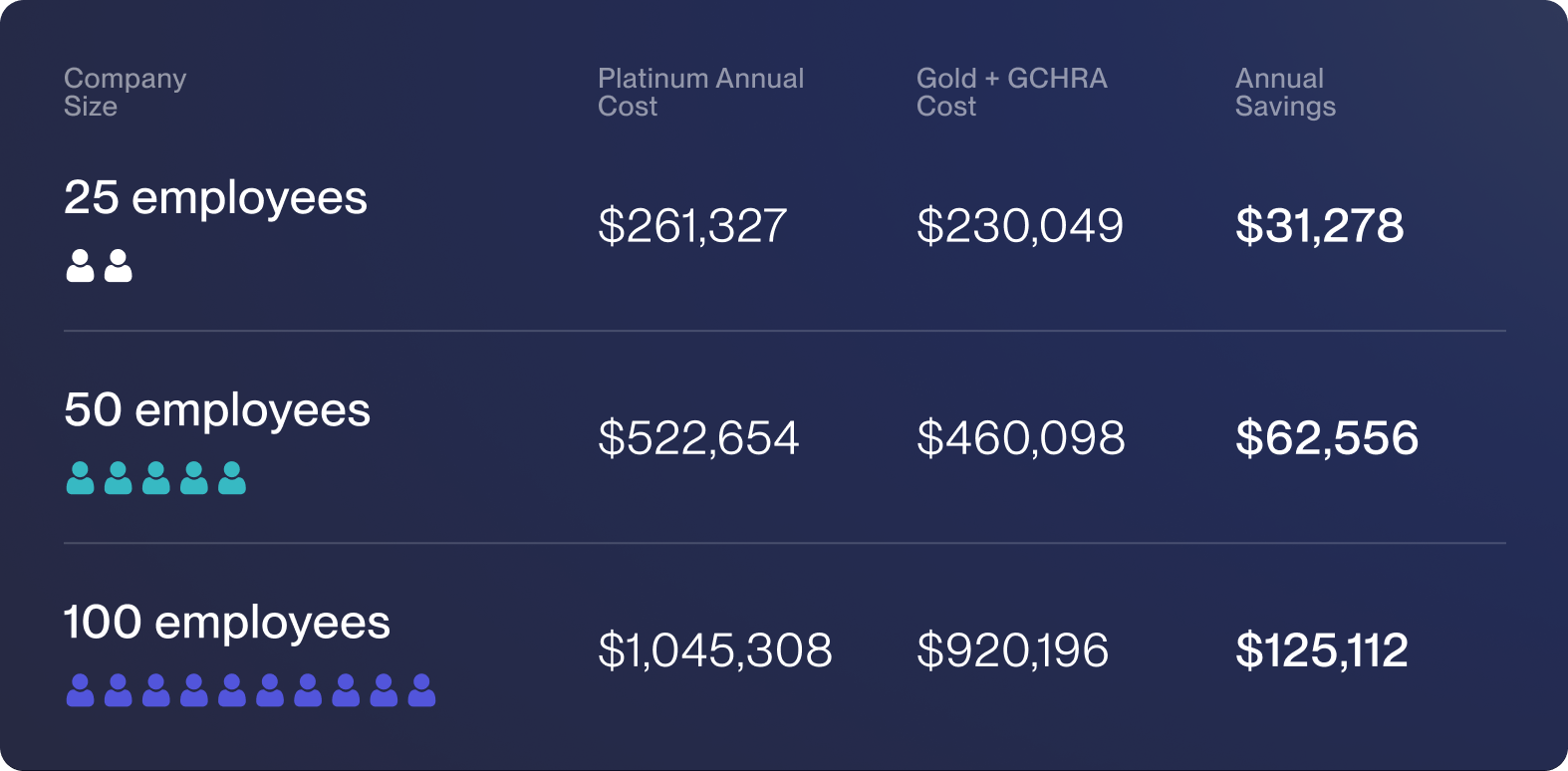

Here's the headline: a 25-person company on a standard Platinum PPO is spending over $261,000 a year on health insurance — and that number went up 6% from the year before. For the third consecutive year, employers are facing cost increases above 5%. For smaller companies with 10–500 employees, it's even worse: those premiums are rising closer to 9% annually if you do nothing.

That's not a rounding error. That's a structural problem.

Over the past five years, the average family premium has gone up 24%. Inflation over the same period? Also around 23%. In other words, health insurance has become its own category of inflation — one you can't opt out of.

But you can't just offer bad benefits

Here's the trap: even as premiums are crushing you, you can't cut coverage without hurting your ability to hire.

Nine out of ten employers say benefits are critical for attracting and retaining talent. For nearly a third of companies, benefits — not salary — are the biggest challenge when it comes to getting candidates to say yes.

And in most knowledge-worker industries, health insurance is table stakes. Your candidate is comparing your offer against a Series B startup with a full benefits package. Or a large company that's been offering Platinum PPO plans for years. If your health insurance looks thin by comparison, you lose the hire.

So you're stuck. Premiums are going up. You can't cut coverage. You just... pay more every year.

At least, that's how most founders think about it.

The dirty secret of expensive health plans: most employees don't use them

Here's something that rarely gets said out loud: if your team skews young and healthy — like most early-stage startups do — a significant portion of your employees will never come close to hitting their deductible.

Think about it. A 26-year-old engineer on your team probably sees a doctor once or twice a year. A PCP visit here, maybe a prescription there. Their total annual healthcare spend might be $200. But you're paying over $10,000 per year to cover them under a Platinum plan with a $0 deductible.

You're buying a Platinum plan to recruit them — because nobody wants to join a company with a high deductible on their offer letter. But once they're on the plan, they're not actually using the thing you're paying so much for.

You're optimizing for the job offer, not for the reality of what your team actually uses.

What if you could keep the low deductible for recruiting — but stop overpaying for employees who don't need it?

That's exactly what a GCHRA does.

GCHRA stands for Group Coverage Health Reimbursement Arrangement. It's a newer benefits model that lets you pair a lower-premium health plan with an employer-funded HRA that covers the deductible difference. The result: employees see a plan with an effectively $0 deductible (same as they'd get on a Platinum), but you're not paying Platinum premiums for it.

Here's how it works in practice:

- You switch from a Platinum PPO to a Gold PPO. The Gold plan has a lower monthly premium, but a higher deductible — say, $500.

- You set up a GCHRA and fund a $500 HRA allowance per employee per year — exactly enough to cover that deductible.

- If an employee hits their deductible, you reimburse them from the HRA. Their out-of-pocket experience is identical to the Platinum plan.

- If an employee doesn't hit their deductible — because they're young and healthy and barely went to the doctor — the unused HRA funds come back to you at the end of the year.

The employee sees a great plan with a $0 effective deductible. You stop overpaying for coverage most of your team isn't using.

What does this actually save?

Let's put real numbers to it. Here's an analysis we ran for a 25-employee company on a UnitedHealthcare Select Plus PPO.

The current plan:

- Platinum 15/90% PPO

- $871.09/month per employee (age 26, single coverage)

- Annual cost: $261,327

- Deductible: $0

The proposed plan:

- Gold 30/500/80% PPO + $500 GCHRA per employee

- $735.58/month per employee — same carrier, same network

- Annual premiums: $220,674

- Maximum HRA budget: $12,500 ($500 × 25 employees)

The premium difference alone is $40,653 per year. Before a single HRA claim is filed, you're already saving money.

Now factor in utilization. Most companies — especially those with younger workforces — see 60–75% HRA utilization in year one. That means employees are only drawing on 60–75% of their HRA budget, and the rest comes back to you.

At the most likely scenario, you're saving over $31,000 a year — around 12% of your total health insurance spend — without changing carriers, without reducing network access, and without touching your employees' effective deductible.

And this scales. Every additional employee on this model saves you roughly $1,250 per year:

So why doesn't everyone do this?

This is the part that surprises most people: the GCHRA isn't a new concept. The regulation enabling it has been in place for years. But almost no one actually offers it — and the reason is operational.

To run a GCHRA properly, you need your payroll, benefits administration, and banking all talking to each other in real time. When an employee files an HRA claim, funds need to move. When an employee leaves mid-year, the math needs to settle correctly. At the end of the plan year, unused balances need to be recaptured.

That requires fintech and HR infrastructure to be genuinely integrated — not just loosely connected through an API or a dashboard. Most benefits brokers can't set it up. Most payroll platforms can't administer it. And most HR platforms don't have the financial infrastructure to move the money.

Every is one of the only platforms that can actually administer a GCHRA end-to-end — because we built banking, payroll, and benefits as a single unified system, not a collection of integrations. The HRA funds live in your Every account. Claims flow through the same system as payroll. Everything reconciles automatically.

The bottom line

If you're offering a Platinum PPO to a team of mostly young, healthy employees, you're almost certainly overpaying. You bought an expensive plan to win job offers — and that's a rational thing to do. But the GCHRA lets you keep the recruiting pitch ("$0 effective deductible, same carrier, same network") while paying a price that actually reflects what your team uses.

For a 25-person company, that's $30,000 back in your budget every year. For a 50-person company, it's over $60,000.

That's not a rounding error either.

If you want to see what the numbers look like for your specific plan and headcount, we're happy to run the analysis — no commitment required.