Cash is oxygen for startups so you have to be very careful where you put it. Some investments are simply off-limits for founders because taking risks with investor capital violates your core fiduciary duty. This guide explains what you cannot do with your company's cash, and why those restrictions exist.

Your Duty as a Founder: Capital Preservation

Your investors entrusted you with capital. Capital preservation is your primary responsibility.

When an investor funds your company, they aren’t hoping to earn returns by having you manage the funds to maximize yield. If they wanted that, they wouldn’t have invested in your company, they would have invested the cash directly themselves.Their mandate is for you to build a large company, not manage a portfolio.

The last thing they want you to do is waste your time optimizing yields. That directly shows you don’t know how to prioritize your time. All your time should be dedicated toward finding product market fit. Time spent on anything else is actually irresponsible.

That being said, the worst thing you can do is accidentally put your cash in an investment vehicle that could cause you to lose the money you put in. This happens when founders don’t pay attention to where they are putting their cash.

Why you can’t blindly trust your bank

This is where most founders go wrong: they outsource their judgment to fintech platforms.

Some platforms understand early-stage treasury compliance and build products accordingly—Every, Mercury, Brex, Ramp among them. But others don't. Some platforms will offer a menu of money market funds, some of them will have higher yields. Most founders want to choose these high yield money markets, because why wouldn’t you want higher yields?

The reason is this: the riskier the asset, the higher the yield. That is how the market works. Risker assets must pay higher interest rates for people to be ok investing in them.

So that higher interest rate money market fund that looked so appealing actually is riskier.

So what can you invest in?

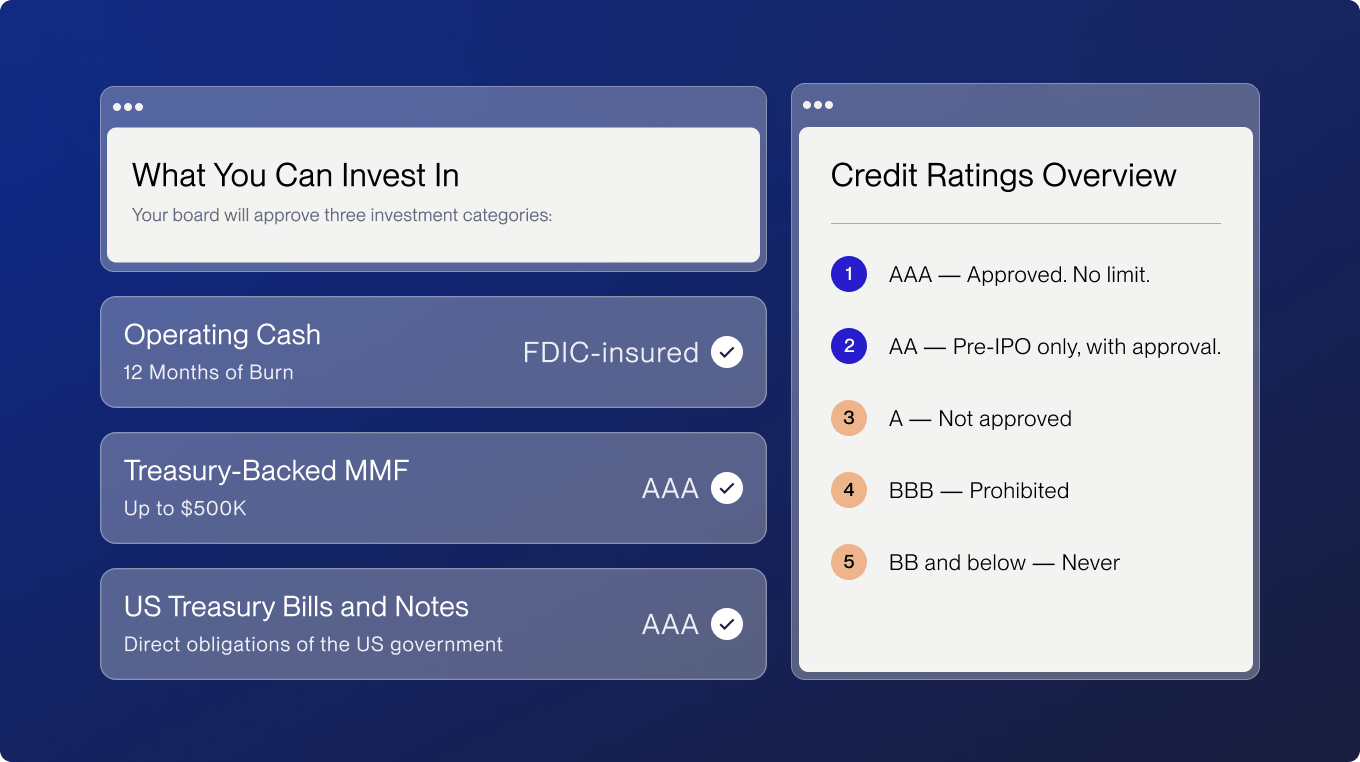

What You Can Invest In: Three Buckets, Three Rules

Your board will approve three investment categories:

Bucket 1: Operating Cash (12 Months of Burn)

Maintain 12 months of monthly burn in FDIC-insured checking accounts. If you burn $200K/month, keep $2.4M here. Prioritize liquidity and access over yield. This is your runway—it is not investable capital.

Credit protection: FDIC insurance (government-backed, not issuer-dependent)

Bucket 2: Treasury-Backed Money Market Funds (Up to $500K)

Money market funds composed exclusively of US Treasury bills and Treasury-backed repurchase agreements.

Credit rating: AAA — Backed by US government obligations. Virtually zero default risk.

If you see a money market that looks higher than the rest of the market, make sure to ask the Credit Rating. This is the key trap I see founders fall into.

Hard limit: SIPC insurance covers $500K per investor per brokerage. Beyond that threshold, funds are uninsured. Do not exceed this limit at any single institution.

Bucket 3: US Treasury Bills and Notes

Direct obligations of the US government, available in maturities from 4 weeks to several years.

Credit rating: AAA — No SIPC exposure because these are direct government debt, not broker-held securities. No practical cap on allocation.

Understanding Credit Ratings and Why AAA-Only Matters

.svg)

The BBB category deserves special attention: this is where yield-chasing most commonly leads. A 3–5% ten-year default rate means a $1M position could return $950K–$970K—or less—in a recession. That's not treasury management. That's taking on risk with someone else's capital.

The Math That Matters

Assume $3M in cash:

- $2.4M → FDIC-insured checking (12 months of burn)

- $500K → AAA Treasury-backed money market fund

- $100K → US Treasury bills

Every dollar is protected. Every position is AAA. Your board moves on.

Now consider a deviation:

- $2.4M → FDIC checking ✓

- $500K → BBB-rated corporate bonds (platform-recommended)

- $100K → Treasury bills ✓

Your board: "Why do we have B-rated corporate bonds?"

You: "They yield 50 basis points more."

Your board: "We gave you $3M to build a company."

The first scenario is unremarkable. The second is a governance failure.

The Bottom Line

Three approved buckets. AAA-only credit exposure. No exceptions.

Your investors didn't fund your company to optimize yield curves with their capital. They funded it to build. Professional treasurers at venture firms, private equity funds, and corporate balance sheets operate under the same standard—not because it's conservative by instinct, but because capital preservation is the discipline that keeps every other option open.

Boring treasury management is the right treasury management.